TIPS Bonds and the Inflation-Tax Paradox

- Maneesh Shanbhag

- Mar 16

- 3 min read

As we approach tax time, instead of writing about tax planning, we are writing about a portfolio tax insight.

Inflation-protected bonds (a.k.a. TIPS) protect against higher inflation by passing through inflation to investors as yield. This dynamic can lead TIPS to outperform traditional nominal bonds during periods of elevated inflation and even equities during inflation surprises, making them potentially the best-performing asset class in a portfolio when inflation is unexpectedly high.

The problem with TIPS, as with most fixed income, is that it is a structurally tax inefficient asset class, because both the coupon and the annual inflation adjustment are taxed as ordinary income. So ironically, as inflation rises, taxable income rises with it, increasing the tax burden.

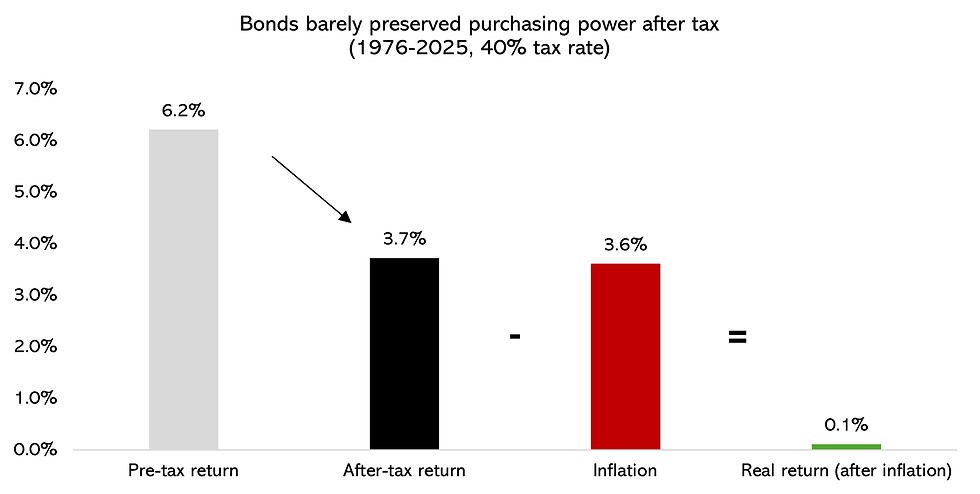

The chart below shows that government bonds barely preserved purchasing power over the last 50 years despite the tailwind of falling interest rates.

Source: Bloomberg, Greenline Partners analysis

For high-net-worth families, the top tax rate on investment income is 40.8%. For historical context, this is the lowest top bracket income tax rate we have had in almost 100 years, per the below chart.

We use the 40.8% rate to show what happens to TIPS as inflation rises in our scenario analysis. It is important to note that in prior periods with higher tax rates, after-tax returns would have been even more negative.

Mechanics of TIPS bonds and after-tax scenario analysis

TIPS pay inflation plus an additional coupon. As inflation changes, so does the income you receive. Over the past almost 30 years, the additional yield over inflation for TIPS has averaged near 2%. We use this value in our scenario analysis.

We want to understand how the net of tax, net of inflation return of TIPS varies as inflation rises. We vary inflation from 0 to 10% and assume a tax rate of 40%. The chart below shows you how the net of tax, net of inflation return of TIPS falls with rising inflation. This means investors are actually losing purchasing power despite holding “inflation-protected” bonds.

Source: Greenline Partners analysis

The problem is that taxes apply to the returns from inflation.

When inflation is low, it is easier for investments to out-earn low inflation, even after taxes. As inflation rises, this presents a headwind to asset prices in general, especially after tax.

The better long-term approach is to own assets where taxes are lower (i.e. dividends and capital gains taxed at 20% instead of 40%) and can be deferred (i.e. equities with long-term capital appreciation).

To be clear, we hold TIPS, ideally in tax-advantaged accounts but even in taxable accounts, as they reduce portfolio drawdowns, and are diversifying to other types of fixed income in inflationary periods. But investors who can tolerate the risk of loss of owning equities may forgo TIPS or any other fixed income.

In summary, TIPS can provide meaningful diversification in the short run, particularly relative to traditional nominal bonds and, at times, equities, as their price movements often differ during inflation shocks. Over the long run, however, the tax treatment erodes the effectiveness of TIPS and therefore should not be relied upon to fully preserve purchasing power, especially during periods of elevated inflation when the tax drag is greatest.

DISCLOSURES: The information contained herein is the property of Greenline Partners LLC and is circulated for information and educational purposes only. There is no consideration given for the specific investment needs, objectives or tolerances of any of the recipients. Additionally, Greenline's actual investment positions may, and often will, vary from its conclusions discussed herein based upon any number of factors, such as client investment restrictions, portfolio rebalancing and transaction costs, among others. Reasonable people may disagree about a variety of factors discussed in this document, including, but not limited to, key macroeconomic factors, the types of investments expected to perform well during periods in which certain key economic factors are dominant, risk factors and various assumptions used. The scenario analysis presented is illustrative, is based on certain assumptions, and is not intended to predict or project future results. Recipients should consult their own advisors, including tax advisors, before making any investment decision. This report is not an offer to sell or the solicitation of an offer to buy the securities or instruments mentioned. No part of this document or its subject matter may be reproduced, disseminated, or disclosed without the prior written approval of Greenline Partners LLC. The scenario analysis presented is illustrative, is based on simplified assumptions, and is not intended to predict or project future results.

Comments