Why the S&P 500 Deserves a Higher P/E Multiple Than History Suggests

- Maneesh Shanbhag

- Nov 19, 2024

- 4 min read

Updated: Nov 7, 2025

Executive Summary

Current Valuation Perspective: The S&P 500's current P/E of 27 may appear high historically, but it doesn't signal a bubble, as today's profitable growth companies differ significantly from past periods that favored growth stocks.

Earnings Quality Analysis: Historical data indicates that unprofitable growth stocks tend to underperform, especially in speculative environments. However, today’s leading growth stocks feature high profit margins and cash flows, marking them as "high quality."

Investment Implications: Despite high valuations, the S&P 500 remains a valuable investment, projected to deliver moderate returns, slightly above bonds. We generally advise investors to favor proven profitability over speculative growth narratives.

Introduction

With the S&P 500 trading at a P/E ratio of 27, it's tempting to say the stock market is in a bubble. From the chart below, by historical standards, this valuation might resemble bubble-like conditions similar to the late 1990s. But while the numbers may initially seem alarming, we see a different story. Today’s market — especially its leading tech companies—offers profitability and quality that shifts how we view these valuations.

We also believe that the concentration risk of the Magnificent 7 is less of an issue than many headlines indicate. The largest S&P 500 positions are only 6–7% of the index each. In comparison, the Dow index only contains 30 stocks, with the largest positions routinely over 8%. Even with this greater concentration, the Dow index has matched the returns of the S&P 500 over the past 50 years with similar volatility.

Today’s Nifty Fifty: Profitable Growth stocks

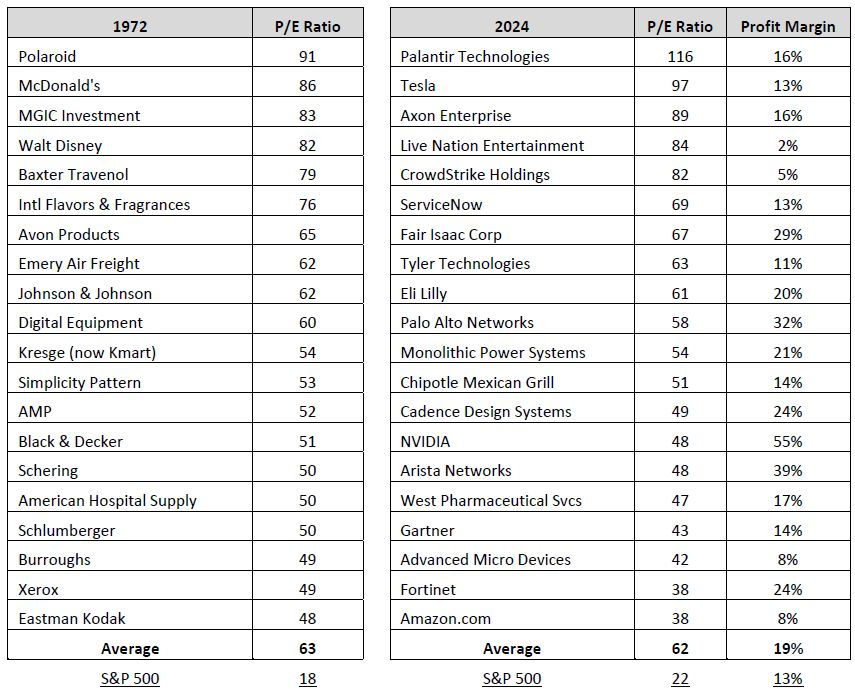

A look back at the 1970s offers one specific case study. During that era, the "Nifty Fifty" stocks, like Coca-Cola and Johnson & Johnson, were viewed as evergreen. Yet, while some thrived, others—like Kodak and Polaroid—suffered greatly when markets turned. In comparison, today’s most profitable tech stocks have shown resilience and strong earnings, distinguishing them from high-growth but low-profitability peers.

We can think of today’s Nifty Fifty as the list of growth stocks within the S&P 500. We show this list below, including their current P/E ratio and profit margin. For comparison we show the actual Nifty Fifty from 1972 and its valuation back then. While the P/E ratio on today’s growth stocks looks high, we can also see they are more profitable than the average company, reducing risk.

Source: YCharts, The Nifty-Fifty Re-Revisited (pomona.edu), Greenline Partners analysis. Data as of 11/04/2024

A history lesson: Growth vs Value, Quality vs Hype

Historically, growth stocks have underperformed the broader market, with unprofitable growth stocks experiencing the steepest declines. The tendency of investors to chase exciting but unproven growth narratives has led to many painful corrections.

The charts below show that cheap (value) stocks have outperformed expensive (growth) ones and quality (high profitability) stocks have outperformed junkier ones (low profitability).

Source: Ken French Data Library. Data from 1963-2024.

Yet, today’s high growth stocks—like the largest technology firms today—don’t fit this pattern. They are, in many ways, the exception. They are highly profitable but also growing quickly and trading at high P/E multiples, showing that they are growth stocks.

Investors’ behavior plays a role here. The excitement around high-growth companies with minimal earnings often drives their valuations too high, resulting in eventual underperformance. Conversely, investors often undervalue companies facing challenges or lower growth, leading these stocks to outperform as they rebound. But today's profitable tech giants like Apple and Microsoft are not simply stories; they have earnings that anchor their valuations.

Valuing Growth Stocks: Profits Over Promises

So, how should we think about valuing today’s high-growth, high-quality stocks? Simply put, profitable growth businesses deserve higher valuations. We put together a table below to put numbers around growth, duration of that growth, and valuation.

At a P/E ratio of 25, a company needs to grow at around 10.7% annually over ten years to justify its price. At 35, the required growth rate climbs to 15.2%. Such growth can be achieved not only through earnings but also via dividends and share buybacks, as long as management uses cash flows wisely.

The table below outlines the required growth for different P/E ratios:

When we see P/E ratios above 50, it implies a need for sustained ~15% growth over long periods—a challenge, especially in the fast-evolving tech sector.

The Investment Takeaway: Focus on Sustainable Returns

So, is the S&P 500 too expensive today? It’s certainly not cheap, but it's far from bubble territory. History suggests that when markets reach high valuations, returns are generally lower in the following years. Still, we don’t believe this warrants avoiding the S&P 500 or trying to time the market. U.S. stocks appear priced to deliver returns modestly above bonds—not sky-high, but respectable.

However, investors should be cautious with speculative, high-growth tech companies that lack earnings. While this exuberance is primarily seen in venture capital, some of it has also spilled into public markets. The advice is simple: avoid hype-driven, unprofitable growth, and invest in companies that generate real profits and demonstrate the potential for sustainable growth.

Ultimately, the market may look expensive by historical metrics, but today’s profitable tech giants set a new standard. By prioritizing quality earnings, we believe investors can still find value—even in a high P/E world.

DISCLOSURES: The information contained herein is the property of Greenline Partners, LLC and is circulated for information and educational purposes only. There is no consideration given for the specific investment needs, objectives or tolerances of any of the recipients. Additionally, Greenline's actual investment positions may, and often will, vary from its conclusions discussed herein based upon any number of factors, such as client investment restrictions, portfolio rebalancing and transaction costs, among others. Reasonable people may disagree about a variety of factors discussed in this document, including, but not limited to, key macroeconomic factors, the types of investments expected to perform well during periods in which certain key economic factors are dominant, risk factors and various assumptions used. Recipients should consult their own advisors, including tax advisors, before making any investment decision. This report is not an offer to sell or the solicitation of an offer to buy the securities or instruments mentioned. No part of this document or its subject matter may be reproduced, disseminated, or disclosed without the prior written approval of Greenline Partners, LLC.

Comments